Introduction: Can One Formula Really Fix Your Finances?

What if managing your entire financial life came down to just three numbers? That’s the promise behind the 50/30/20 rule, one of the most widely recommended budgeting frameworks in personal finance today. It’s simple enough to calculate on a napkin, yet structured enough to guide decades of financial decisions.

But does a one-size-fits-all formula actually hold up against today’s economic realities, record household debt, rising rents, and a savings rate hovering near historic lows? This guide breaks down exactly what the 50/30/20 rule is, where it came from, how to apply it step by step, and where it falls short so you can decide whether it’s the right framework for your money.

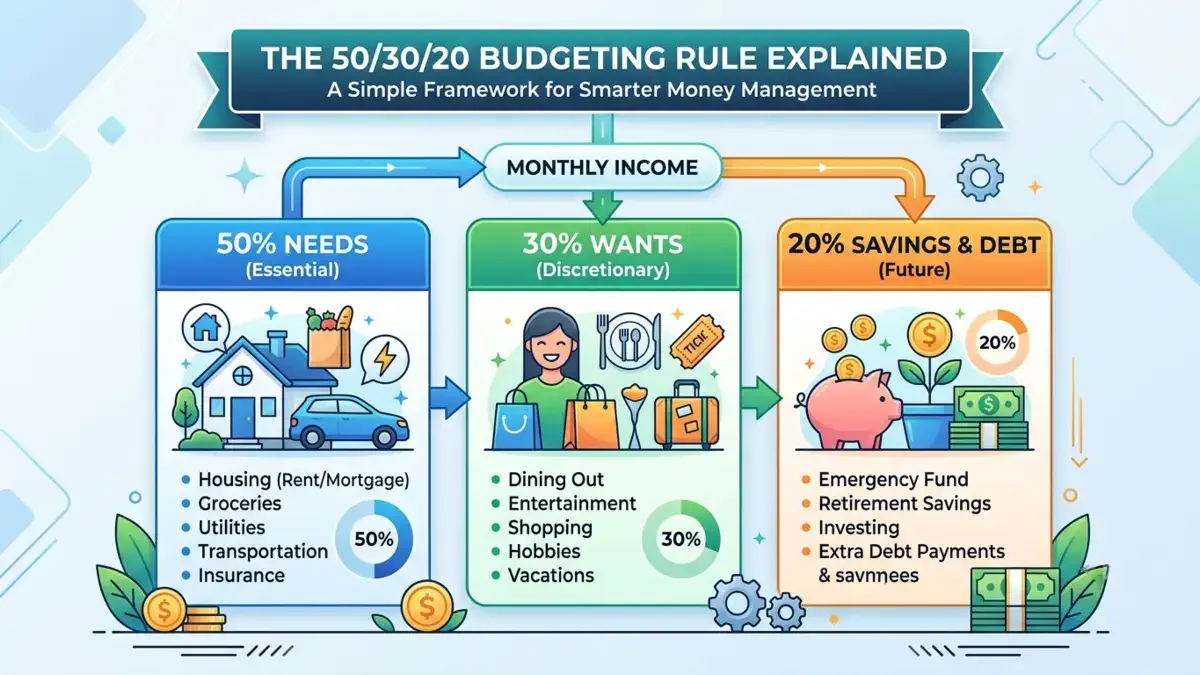

What Is the 50/30/20 Rule?

The 50/30/20 rule is a budgeting method that divides your after-tax (take-home) income into three spending categories:

- 50% for needs: housing, groceries, utilities, insurance, transportation, and minimum debt payments

- 30% for wants dining out, entertainment, subscriptions, travel, and other discretionary spending

- 20% for savings and extra debt repayment, emergency funds, retirement contributions, investments, and any debt payments beyond the required minimum

The framework was popularized by Senator Elizabeth Warren in her book “All Your Worth,” which laid out this three-category approach to after-tax income allocation. Its appeal lies in its simplicity: rather than tracking dozens of micro-categories, you only need to manage three broad buckets.

Why the 50/30/20 Rule Has Stayed Popular

It Removes the Guesswork

Traditional budgeting often fails because it’s too granular; tracking twenty different spending categories becomes tedious and is easy to abandon. The 50/30/20 rule solves this by simplifying decision-making into three percentages that apply to nearly any income level.

It Builds Savings Into the Plan by Default

Unlike budgets that treat savings as “whatever is left over,” the 50/30/20 rule assigns a fixed 20% to savings and debt repayment from the start. This matters significantly given the current financial landscape: the U.S. household saving rate sat at just 3 percent in mid-2026, and 43 percent of Americans couldn’t cover a $1,000 emergency expense from savings alone. A framework that forces savings into the equation, rather than leaving it optional, directly addresses this gap.

It Adapts to Any Income Level

Because the rule works in percentages rather than fixed dollar amounts, it scales automatically whether you earn $40,000 or $140,000 a year, making it one of the more flexible budgeting frameworks available.

How to Apply the 50/30/20 Rule: Step by Step

Step 1: Calculate Your After-Tax Income

Start with your take-home pay, the amount that lands in your bank account after taxes, retirement contributions, and other payroll deductions.

Step 2: Allocate 50% to Needs

This category should only include true essentials:

- Rent or mortgage payment

- Utilities (electricity, water, internet)

- Groceries

- Health insurance and minimum insurance premiums

- Transportation costs (car payment, gas, or transit pass)

- Minimum payments on existing debt

Step 3: Allocate 30% to Wants

This is your lifestyle category spending that improves quality of life but isn’t strictly necessary:

- Dining out and takeout

- Streaming subscriptions and entertainment

- Travel and vacations

- Hobbies, shopping, and personal upgrades

Step 4: Allocate 20% to Savings and Debt Payoff

This includes:

- Emergency fund contributions

- Retirement account contributions (401(k), IRA)

- Extra payments toward credit cards, student loans, or other debt beyond the minimum

- Investment contributions

Step 5: Track and Adjust Monthly

A budget is only useful if it’s reviewed. Track actual spending against your 50/30/20 targets each month and adjust categories where you consistently overspend or underspend.

Where the 50/30/20 Rule Runs Into Trouble: The Housing Problem

The biggest criticism of the 50/30/20 rule centers on its housing assumptions. The rule lumps rent or mortgage payments into the broader 50% “needs” category, but in many U.S. markets, rent alone now consumes nearly that entire share.

A separate but closely related guideline, the 30% rule for housing, holds that no more than 30 percent of gross income should go toward rent and utilities, a standard that traces back to the 1969 Brooke Amendment governing public housing. Yet current market data shows that the benchmark is increasingly out of reach for a large share of renters. Academic researchers at the Harvard Joint Center for Housing Studies have closely examined whether the long-standing 30% income standard for housing affordability remains a reliable benchmark in today’s market, finding that its usefulness varies considerably depending on income level and local cost of living.

In practice, this means:

- Renters in high-cost metro areas may find that housing alone consumes 40–50% of take-home pay, leaving little room for other “needs” within the 50% bucket.

- Households carrying significant existing debt, the average U.S. household now carries $10,895 in revolving credit card debt, may find their minimum debt payments alone strain the needs category before housing and groceries are even factored in.

- The rule assumes a level of income stability and cost-of-living consistency that doesn’t reflect every household’s reality.

Adjusting the Rule for Real-World Budgets

Financial educators increasingly recommend treating the 50/30/20 split as a flexible starting point rather than a rigid formula. Useful adjustments include:

- Shifting to 60/20/20 or 60/30/10 in high-cost areas, where housing alone justifies a larger “needs” allocation

- Prioritizing debt payoff by temporarily increasing the savings/debt category beyond 20% if you’re carrying high-interest credit card balances

- Using net (after-tax, after-retirement-contribution) income rather than gross income for more realistic percentage calculations

- Building in a “miscellaneous” buffer within the wants category for irregular costs like gifts or annual subscriptions

50/30/20 vs. Other Budgeting Methods

It’s worth understanding how the 50/30/20 rule compares to other widely used approaches:

- Zero-based budgeting assigns every dollar a specific job until income minus expenses equals zero, offering more precision but requiring more ongoing tracking than 50/30/20.

- The envelope system allocates cash to specific spending categories and stops spending once an envelope is empty useful for curbing overspending but less flexible than percentage-based methods.

- Pay-yourself-first budgeting prioritizes savings contributions before any other spending, similar in spirit to the 20% savings target in 50/30/20, but applied more aggressively.

For many households, the 50/30/20 rule serves as an effective entry point before graduating to a more detailed system like zero-based budgeting.

The Bottom Line: Is the 50/30/20 Rule Right for You?

The 50/30/20 rule remains one of the most accessible ways to bring structure to your finances without the burden of micromanaging every expense category. Its built-in savings allocation is particularly valuable at a time when over 84 percent of self-reported budgeters say budgeting has helped them avoid or pay off debt. However, the rule works best as a flexible guideline rather than an inflexible law, especially for renters in high-cost markets or households carrying significant debt, where the percentages may need real adjustment to reflect actual financial circumstances.

Ready to put the 50/30/20 rule into practice? Calculate your after-tax income today, sort last month’s spending into the three categories, and identify the one adjustment, whether trimming discretionary spending or boosting your savings rate, that will move you closer to your financial goals this month.