Introduction: The Single Habit Separating Financial Stress From Financial Stability

What if one simple habit could be the difference between living paycheck to paycheck and building lasting wealth? It sounds almost too simple, yet the data backs it up. Nearly seven in ten Americans now report living paycheck to paycheck, a figure that has climbed steadily since 2022, while the share of households tracking a formal budget has grown. That contrast is no coincidence; it points to budgeting as one of the most reliable tools for navigating an unpredictable economy.

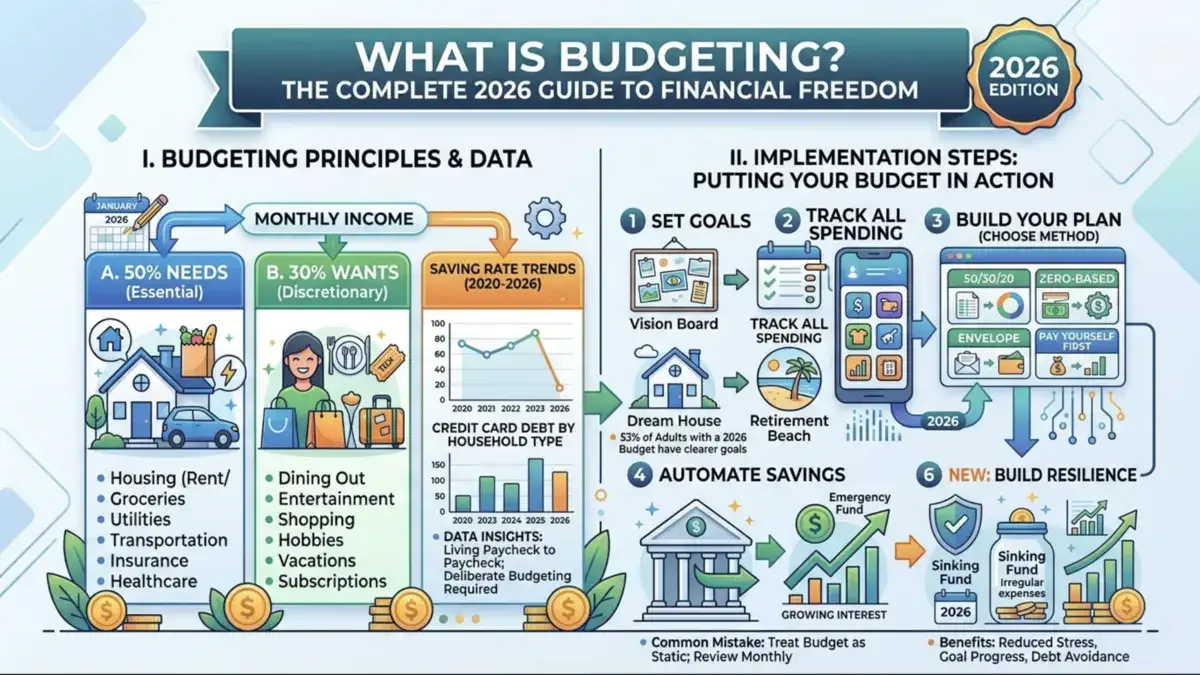

So, what is budgeting, exactly? At its core, budgeting is the process of creating a plan for how you will earn, spend, save, and invest your money over a specific period, typically a month. It is not about restriction for its own sake; it is about intentionality. A budget tells every dollar where to go before it’s spent, replacing financial guesswork with a clear, actionable roadmap.

This guide breaks down what budgeting really means, why it matters more in today’s economic climate than perhaps any time in recent memory, the most effective budgeting methods available, and how to choose a system that actually sticks.

Why Budgeting Matters More in 2026 Than Ever Before

The Cost-of-Living Squeeze Is Real

Inflation may have cooled from its post-pandemic peak, but household budgets are still under pressure. Persistent inflation has eroded real purchasing power, while elevated housing costs and rising consumer debt burdens continue to squeeze disposable income. This pressure shows up clearly in the national savings data: by mid-2026, the U.S. household saving rate held at just 3 percent, a fraction of the levels seen during the pandemic-era savings surge.

Put simply, Americans are keeping less of every dollar they earn, which makes deliberate budgeting less of a “nice to have” and more of a financial necessity.

The Credit Card Debt Trap

Without a budget, it becomes far easier to lean on credit to cover the gap between income and expenses, and the numbers show this happening in real time. As of early 2026, the average American consumer carried $6,595 in credit card debt, contributing to a national total of roughly $1.252 trillion in outstanding credit card balances. At the household level, revolving credit card debt averaged $10,895 as of March 2026, and nearly half of cardholders, 47 percent, carried a balance from month to month as of late 2025.

This matters because credit card interest compounds quickly. Carrying a balance at today’s rates can mean paying thousands of dollars in interest over time, money that could otherwise go toward savings, investments, or debt freedom. A working budget is one of the most effective ways to interrupt this cycle before it starts.

The Emergency Fund Gap

Perhaps most concerning, many households remain financially exposed to even minor disruptions. A recent national survey found that more than two in five Americans, 43 percent, could not cover a $1,000 emergency expense using savings alone, and roughly a third said they lacked enough savings to cover even one month of living expenses. Budgeting directly addresses this vulnerability by building emergency savings into the plan from the start, rather than treating it as an afterthought.

The Core Components of a Budget

A core component of a budget rests on four pillars. Understanding each one is the foundation for building a plan that works for your specific financial situation.

- Income – All money coming in: salary, freelance earnings, side-business revenue, or investment income.

- Fixed expenses – Costs that stay relatively constant each month, such as rent or mortgage payments, insurance premiums, and loan payments.

- Variable expenses – Costs that fluctuate, including groceries, utilities, entertainment, and discretionary spending.

- Savings and debt repayment – Money allocated toward emergency funds, retirement accounts, investments, and paying down existing debt.

The goal of budgeting is to balance these four categories so that income covers obligations while still leaving room for savings and financial goals, ideally without relying on credit to bridge any shortfall.

Popular Budgeting Methods Explained

There is no single “correct” way to budget. The right method depends on your income structure, financial goals, and personal preferences for structure versus flexibility.

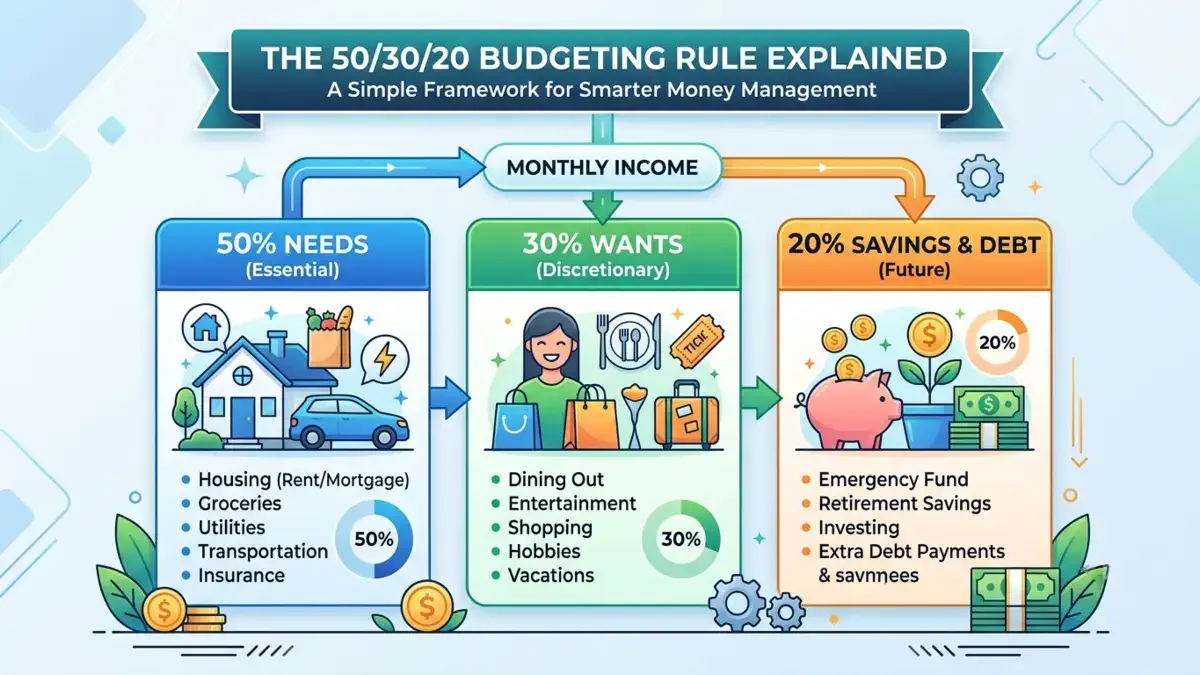

The 50/30/20 Rule

This widely used framework allocates after-tax income into three broad buckets: 50% toward needs (housing, utilities, groceries), 30% toward wants (dining out, hobbies, entertainment), and 20% toward savings and debt repayment. Its simplicity makes it a popular entry point for beginners.

Zero-Based Budgeting

In this method, every dollar of income is assigned a specific job, whether that’s an expense, a savings goal, or debt repayment, until income minus allocations equals zero. This approach offers maximum control and is especially useful for people who want full visibility into where their money goes.

The Envelope System

A cash-based method in which spending categories are assigned physical (or digital) “envelopes” containing a fixed amount of money. Once an envelope is empty, spending in that category stops for the month. This tactile approach is highly effective for curbing overspending in discretionary categories.

Pay-Yourself-First Budgeting

Rather than starting with expenses, this method prioritizes savings and investment contributions, allocating the remaining income to spending. It’s particularly effective for people focused on aggressive saving or long-term wealth-building goals.

Choosing the Right Budgeting Tool

How people actually build and maintain their budgets varies significantly, and the data show real generational and behavioral differences in tool preferences.

- Spreadsheets remain the most widely used budgeting tool overall, used by 35 percent of U.S. adults, including nearly half of adults aged 18–24.

- Budgeting apps are used by 16 percent of adults overall, rising to 34 percent among 25–34-year-olds, reflecting a generational shift toward automated, mobile-first money management.

- Bank-provided financial tools are used by roughly 17 percent of adults, offering a middle ground between manual tracking and full automation.

- Pen-and-paper tracking still appeals to a meaningful share of budgeters who prefer a tactile, low-tech approach.

There’s encouraging momentum here, too: the share of U.S. adults who report having a 2026 budget rose to 53 percent, up from 46 percent the previous year, with similar growth confirmed by other national surveys. The percentage of Americans who say they follow a monthly budget has climbed from 47 percent in 2021 to 53 percent in 2026, with the largest gains coming from Gen Z and middle-income households.

Common Budgeting Mistakes to Avoid

Even well-intentioned budgets fail when certain pitfalls go unaddressed. Watch out for these common missteps:

- Being unrealistic about discretionary spending underestimates how much you actually spend on dining out, subscriptions, or impulse purchases.

- Failing to plan for irregular expenses, such as annual insurance premiums, car maintenance, or holiday spending that don’t occur monthly, but still need a sinking fund.

- Treating the budget as static income and expenses change, a budget reviewed only once a year quickly becomes outdated.

- Skipping the emergency fund, prioritizing other goals while leaving no buffer for unplanned costs, often forces reliance on credit cards.

- Abandoning the system after one bad month of budgeting is iterative; one overspent category doesn’t mean the system has failed.

The Real Benefits of Budgeting

The payoff of consistent budgeting is well documented. Among Americans who maintain a regular budget, the most common motivations include ensuring enough money is available for essentials like food, rent, and bills, and increasing overall savings. Critically, the practice appears to work: among self-reported budgeters, over 84 percent say budgeting has helped them either avoid debt or pay it off, and nearly all respondents in the same survey called budgeting more important now than ever before.

Beyond debt avoidance, budgeting delivers compounding benefits over time:

- Reduced financial stress through greater visibility and control over cash flow.

- Faster progress toward goals like home ownership, retirement, or paying off student loans.

- Improved credit health by avoiding the high-interest revolving debt that weighs down so many household balance sheets.

- Greater resilience to income shocks, job loss, or unexpected expenses.

Conclusion: Your Budget Is the Foundation of Every Financial Goal

Budgeting is not a punishment or a sign of financial trouble; it’s the operating system for every other financial decision you’ll make, from building an emergency fund to investing for retirement. In an economic environment marked by elevated living costs, record credit card balances, and thin savings cushions, a clear and consistently maintained budget is one of the most powerful tools available for protecting your financial future.

The data is unambiguous: people who budget are more likely to avoid debt, build savings, and feel confident about their financial trajectory. Whether you choose the simplicity of the 50/30/20 rule, the precision of zero-based budgeting, or the discipline of the envelope system, the most important step is to start and review your plan regularly as your income and goals evolve.

Ready to put a budget into action? Start by tracking last month’s spending, choose a method that fits your lifestyle, and set one specific savings goal to work toward this month. Small, consistent steps compound into significant financial progress over time.